When the Club of Rome published Limits to Growth in 1972, the economist Kenneth Boulding remarked to the US Congress that ‘anyone who believes exponential growth can go on forever in a finite world is either a madman or an economist’. At first, it seems like a disparaging reflection on his own profession. But beneath Boulding’s irony lies an important insight into what Greta Thunberg more recently called the ‘fairytales of eternal economic growth’.

As global leaders meet in Glasgow to work out how to meet the commitments of the 2015 Paris Agreement, the underlying growth-based economic model has come under renewed scrutiny. Many will push back on this, but the raw numbers of climate change show why we need engagement at the highest level on post-growth economics.

First off, it’s worth noting that when economists contend that growth can go on forever, it’s because their preferred measure of growth – gross domestic product or GDP – is often measured in monetary rather than in material terms. Carbon emissions and economic growth are separable, on this view. By ‘decoupling’ one from the other, we ought to be able to escape the finite limits that nature seems to impose.

It is vital to distinguish here between relative and absolute decoupling. The former refers to a decline in the carbon intensity of economic output. The latter to an absolute fall in carbon emissions that continues even when output rises. Put simply, relative decoupling is about doing things more efficiently. And since efficiency is one of the things that capitalism is supposed to be good at, decoupling has a familiar logic and a clear appeal to those hoping growth can continue indefinitely.

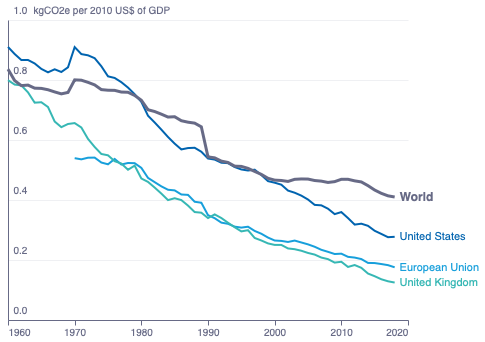

It is easy to find evidence for relative decoupling, even at the global level. For instance, the carbon intensity of the global economy fell from about 800 grams of carbon dioxide per dollar (gCO2/$) in 1960 to a little more than 400 gCO2/$ today, a decline of almost 50% in little over half a century.

Figure 1: Emissions intensity of GDP (Source: World Bank Development Indicators)

But relative decoupling is barely half the story. For efficiency to lead to an absolute fall in emissions, the carbon intensity of the economy must decline faster than economic output rises. What’s more, if the economy continues to grow forever, then efficiency must outpace growth indefinitely. And it must do so fast enough to reach net zero before time runs out to keep global temperatures below 1.5°C or even 2°C above the pre-industrial average.

The evidence for that possibility isn’t compelling. The fastest efficiency gains the advanced economies ever made was an average decline in carbon intensity of around 3%. That happened in the years immediately following the oil crises of the 1970s. Today, the rate of decline is barely 1% each year. This is far below the 14% that is needed to avoid runaway climate change.

In the meantime, global carbon emissions are more than three times higher today than they were in 1965 despite the efficiency improvements since then. Efficiency moved on. But scale outran it. And now we find ourselves running out of time to ensure a liveable climate for our children.

A recently leaked draft report from Working Group III of the IPCC’s 6th Assessment supports this view. The paper acknowledges that there is little or no room for further economic growth and even suggests that we need to move away from the current capitalist model of economics.

There’s no doubt that’s a scary proposition. Only a few economists – and even fewer politicians – have challenged the primacy of economic growth. Fewer still have begun to think about how a post-growth economics would work. We’ve been so convinced that growth can go on forever that we’ve built almost all of our financial and political institutions around that assumption.

But being frightened to scare the horses is no way to win the race against climate change. Einstein had a different definition of madness from Boulding. Insanity, he said, was doing the same thing over and over and expecting a different outcome. So perhaps it’s time to put post-growth economics at the heart of the COP26 negotiations.

Where can I find out more?

- Post-growth: Life after capitalism

- Prosperity without growth: Foundations for the economy of tomorrow

- Unraveling the claims for (and against) green growth

- The state in the transformation to a sustainable postgrowth economy

This blog first appeared on the Economics Observatory website. (Licensed under CC-BY-NC-ND 4.0). Header image: Courtesy of by Red Zeppelin/unsplash.com.